While much has been written about the demise of BlackBerry (RIM), I'm unsatisfied with the common Innovator's Dilemma argument. Just as the book Freakonomics taught us that economic puzzles can't simply be explained by "supply & demand", why tech companies fail is more nuanced than an innovator's dilemma argument.

My theory picks up on the same premise as the book Freakonomics that asserts many economic problems are really human ones; people are driven by incentives, sometimes running counter to their own well being. Here, I look at how RIM simply acted in a way aligned with their incentives, as a Canadian public company.

RIM stock was held disproportionately by Canadian pension funds

Recall that BBRY (formerly RIMM) is listed on the Toronto Stock Exchange (TSX), and thus held -- disproportionately to its US competitors --- by Canadian investors. Big Canadian pension funds like Jarislowsky Fraser Ltd, and McLean Budden, tend to be excellent quantitative portfolio managers, whose goal is to provide steady long-term gains. Their portfolio managers are likely to heavy up "stable" securities, and then allocate a smaller proportion of those assets to "higher beta" holdings -- not unlike the strategy of venture capital limited partners (LPs).

RIM was the only game in town...or the country

Prior to 2006, there were laws about "foreign content ownership" placed on the average Canadian's retirement fund (RRSPs), such that in order to receive favorable tax breaks, a large proportion of holdings had to be placed in Canadian assets.

So, if you looked at the Canadian market, what do we really have? Financial institutions and natural resources. Therefore, if you're a quantitative portfolio manager looking for bigger gains, you need to diversify from holdings of potash and gold and into higher beta holdings like tech stocks. With the former Canadian darling tech company Nortel dying, RIM was a juggernaut. So that's where investors went -- and frankly because there weren't that many other options more money in. This in turn raised the RIM stock price price, which in turn poured more money in, and created a virtuous cycle.

Even when foreign content ownership laws changed in 2006, these investors could have rolled out of RIM and put their money into offshore holdings, but Canadian investors tend to be more risk averse, and lack the long-term history of successful high-tech investing. Moreover, RIM had recently emerged from a long lawsuit with patent troll NTP, and the stock was still rolling, so why leave?

The stock rose (or was steady) while the industry changed around it

In Oct 2007 RIM was the most valuable company in Canada (market cap of $68 billion) at one point, with its shares up 150% since the start of the year. So while it is easy, in hindsight, to say that RIM was either unwilling, or incapable (or both) to respond to the iPhone, RIM's stock price was totally unaffected by its launch -- so investors didn't care. Moving forward to 2008 and 2009 when the rest of the economy was in freefall, who wanted to put money into banking? So Canadian investors heavied up on RIM, the "safe" investment. Moreover, the company's growth in emerging markets was into high gear, and subscriber numbers were still growing overall.

This chart shows the company's stock relative to to the Nasdaq over the last 5 years, which shows it held up pretty well for a long time. BTW, that big drop can be explained by a stock split.

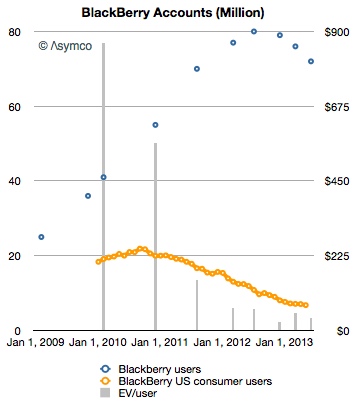

Moreover, the "fundamentals" of the company might still be seen as strong, from a purely quantitative perspective. This next chart shows strong overall user growth; however, really coming from lower margin, emerging markets.

The rising stock price buoyed (false) confidence

So no one was really leaving the party, and announcements like their new OS coming "any day", gave some signs of hope. Bottom line, the stock remained ok while the company's core was crumbling. Therefore, with stock based incentive compensation, management was effectively "rewarded" for their actions. This created a mindset whereby they could dismiss Apple & Google as "better marketers", and their competitor's products as "toys" vs. "tools" .

Likely, this inward focus created a false sense of confidence, and must have made management meetings look like a Mad Hatter's Tea Party. So, by the time the lights went on it was too late...and we all know how the story ended.

Innovator's Dilemma is an easy, but incomplete, answer

So, there are many fingers to point and excuses to make, such as the company's co-CEOs, perhaps arrogance, perhaps ineptitude, or perhaps distraction. But, I'll contest the reason there was never a burning platform memo, was that they were completely blindsided.

Instead, the quant-driven institutional investors could not fully appreciate the dynamics of this industry, and didn't realize the next big thing looked like a toy. So, by the time the Board acted in 2012, it was too late, they brought in the wrong guy, and in all likelihood, he never had a fighting chance.

What happens next is anyone's guess...if anyone still cares.

Epilogue

There are rumors swirling that pension funds will save the company, which is quite ironic since what killed the company, will attempt to save it.

Related posts on this blog

From 2009: Will RIM be this decade’s Nortel?From 2010: 10 places to look for mobile’s next killer app